Key Takeaways |

|---|

|

"If the textbook were enough, everyone would pass. It isn't. And most people find out too late."

Stop. Before you read another chapter, before you highlight another definition — read this first. The UBC Sauder course is 21 chapters of content that assumes you'll figure out the rest.

Most students don't. Not because they're unprepared, but because the exam operates on a logic nobody ever teaches directly.

These 11 secrets are the hidden map behind the official material. The students who pass aren't smarter. They aren't working harder. They just knew this going in. Now you will too.

How to Get Your Mortgage Broker License in BC

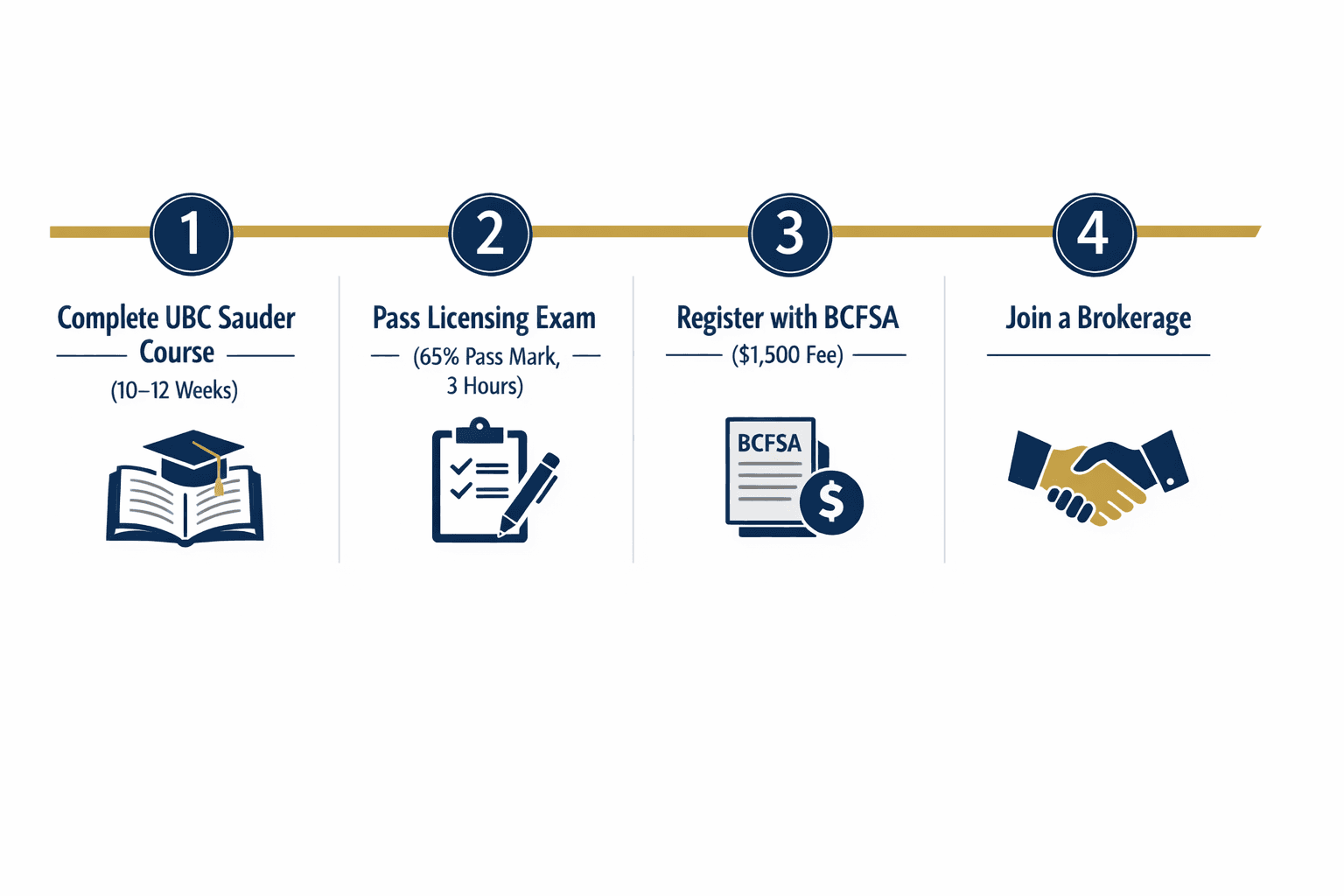

Before we jump into knowing the secrets, let's answer the most common question we get from prospective students. Here is the exact four-step licensing path in British Columbia:

The Licensing Roadmap

Complete the UBC Sauder Mortgage Brokerage in British Columbia course. This is the only government-approved course for BC licensing. It has 21 chapters and takes most self-study students 10–12 weeks to complete. With structured support, our students do it faster and smarter.

Pass the 3-hour licensing exam with a minimum score of 65%. This is where most self-study candidates stumble — not because they're not smart, but because they studied the wrong things.

Register with BCFSA as a Submortgage Broker (approximately $1,500 in fees). BCFSA is BC's financial services regulator — your licence comes from them, not UBC.

Join a licensed brokerage. This is the most underestimated step. The brokerage you join in year one determines the quality of your mentorship, your access to lenders, and your income ceiling. We'll return to this in Secret 11.

2026 Update: Under the incoming Mortgage Services Act (MSA), "Submortgage Broker" is being renamed to "Mortgage Broker."

What 11 Secrets Will a BC Mortgage Broker Course Reveal?

Each secret below is either a concept you've heard of but never truly understood — or something you won't find explained this way anywhere else

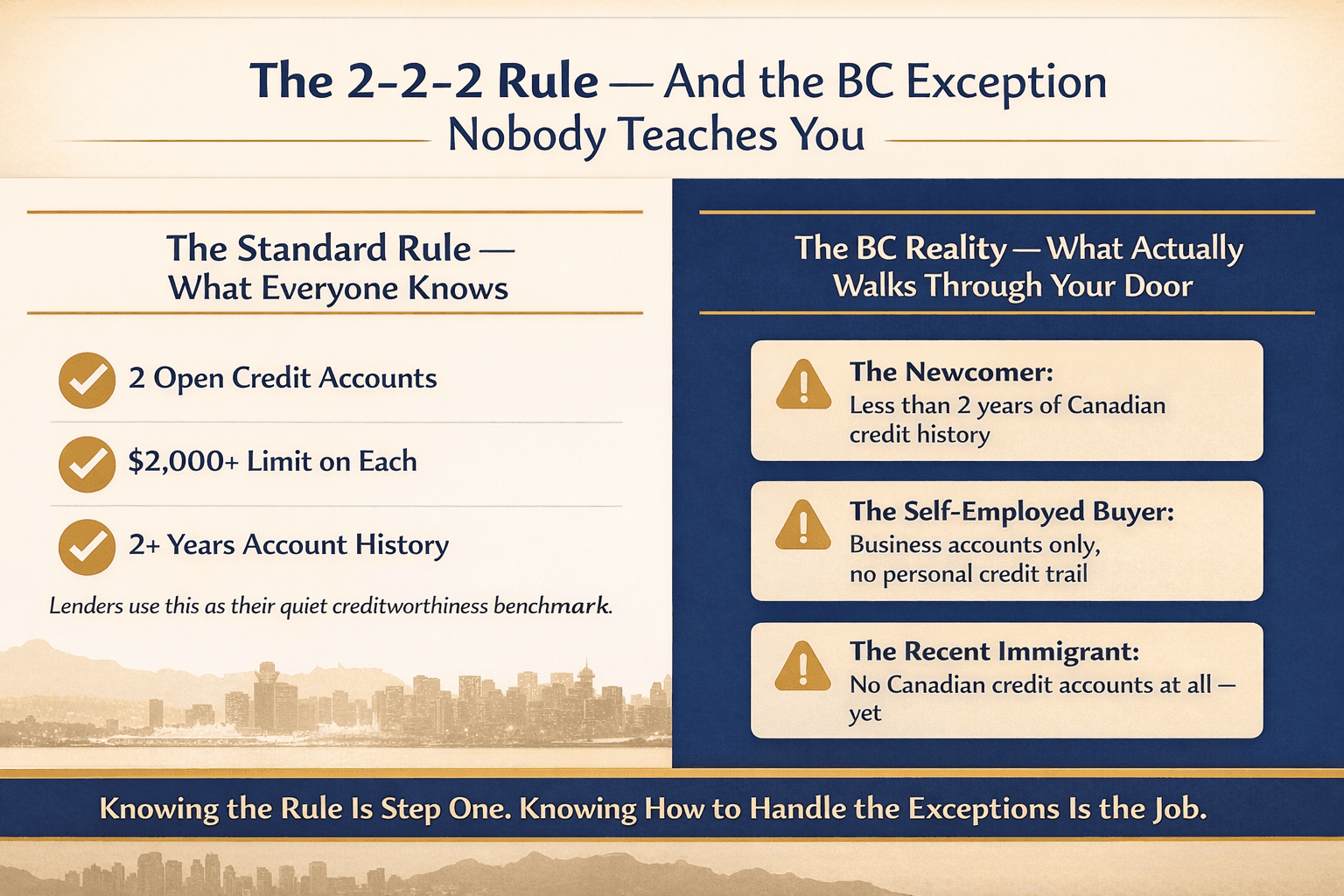

Secret 1 — The 2-2-2 Rule… And the BC Exception Nobody Mentions

What everyone knows is that there are two open credit accounts, each with a $2,000+ limit, that have been held for at least two years.

But the thing that nobody teaches you is how this rule breaks down in real BC client files.

In Metro Vancouver and Surrey, a large portion of first-time buyers are newcomers or self-employed. Many haven't held a Canadian credit for two years.

Many use business accounts rather than personal ones. Knowing the rule is not enough. Knowing how to handle a client whose profile doesn't fit is a skill.

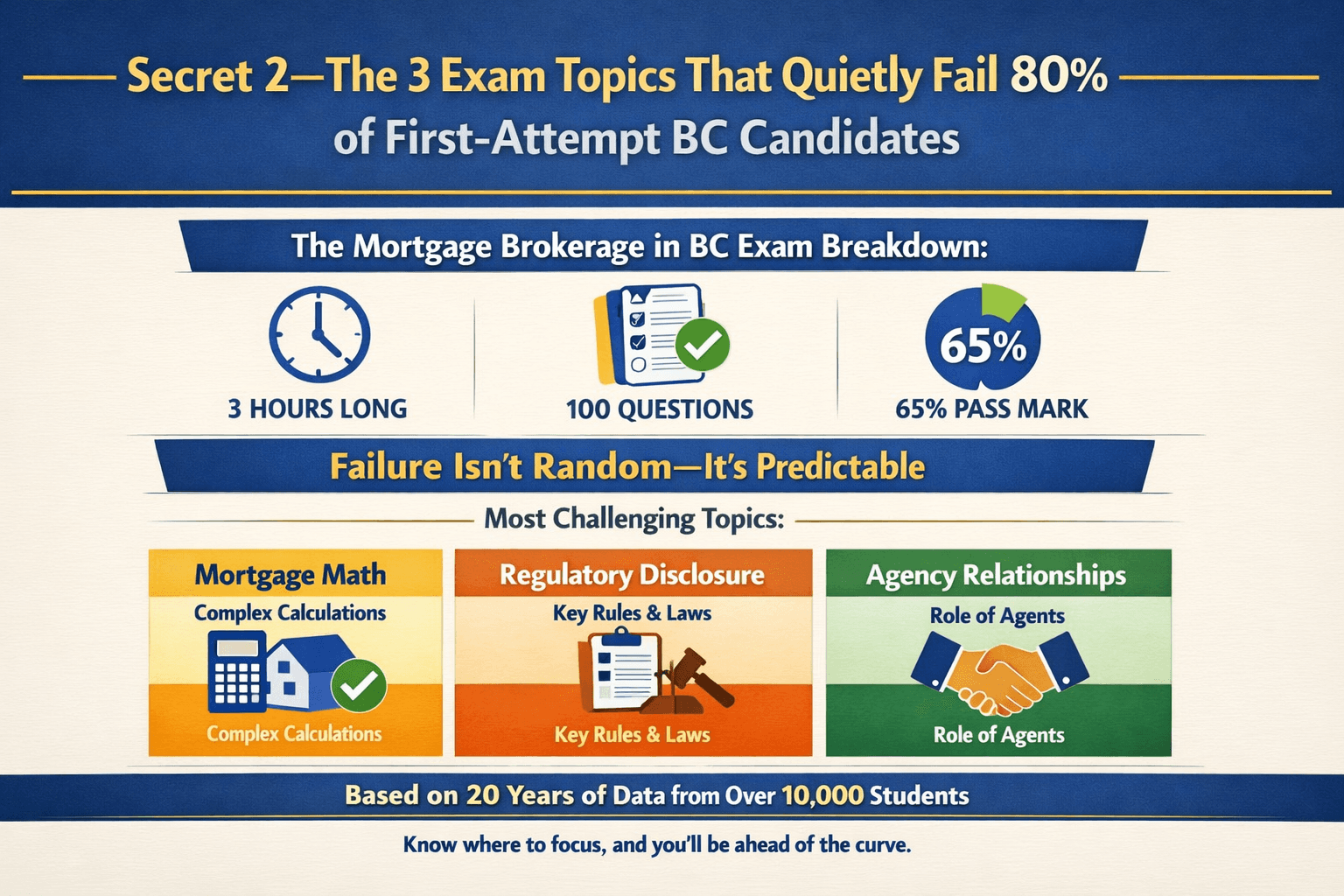

Secret 2 — The 3 Exam Topics That Quietly Fail 80% of First-Attempt BC Candidates

What most students don't realise is that not all 21 chapters carry equal exam weight. Failure isn't random —The Mortgage Brokerage in BC exam is three hours long, contains 100 multiple-choice questions, and requires a passing grade of 65%. UBC Sauder School of Business Knowing which of those 100 questions cluster around the same three topic areas changes how you prepare entirely.

Treating every chapter the same is the single most common mistake. Know where the exam consistently bites before you walk in, and a first-attempt pass becomes significantly more achievable.

Note: This isn't theory. It is 20 years of tracking 10,000 people through the same exam and noticing where the floor drops out.

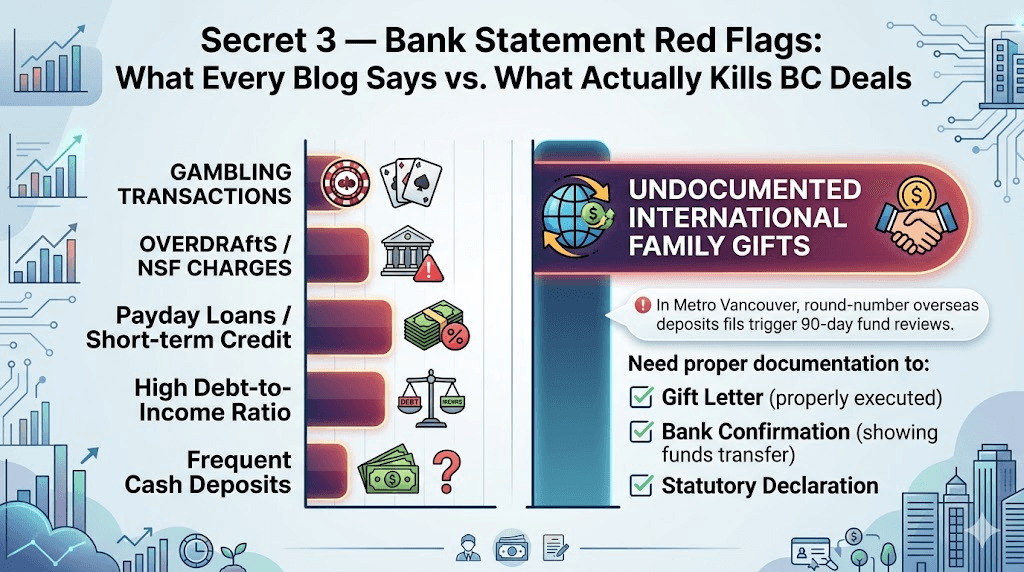

Secret 3 — Bank Statement Red Flags: What Actually Kills BC Deals

You already know the basics — gambling transactions, overdrafts, and payday loans raise red flags for lenders. But here is what actually kills BC deals: an international family gift without proper documentation.

In Metro Vancouver, round-number overseas deposits trigger unexplained fund reviews requiring a full 90-day paper trail. If your client's down payment is coming from family abroad, which is common across BC's buyer demographic, you need a proper gift letter, bank confirmation, and sometimes a statutory declaration ready before the lender ever sees the file.

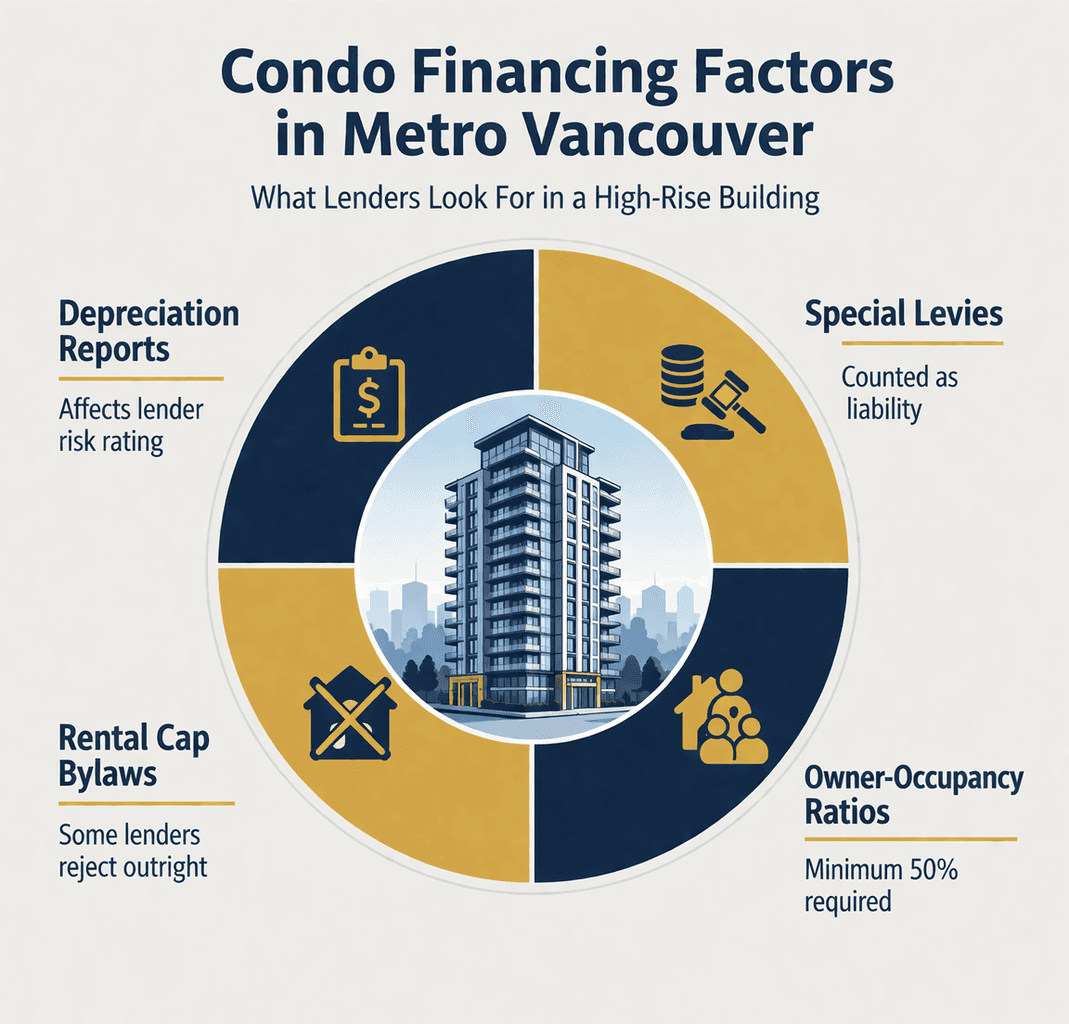

Secret 4 — Why BC's Strata Market Creates Mortgage Complications No Other Province Faces

Most mortgage courses teach standard approval criteria. They don't teach this: strata-titled properties make up a dominant share of Metro Vancouver's housing stock — a concentration found nowhere else in Canada. Lenders treat strata units completely differently from freehold properties.

Depreciation reports, pending special levies, rental restriction bylaws, and minimum owner-occupancy ratios all affect whether a file gets approved. A $900,000 Surrey condo can fail financing not because of the buyer's income or credit, but because the strata corporation has a rental cap that the lender won't accept.

Most new brokers discover this mid-deal. Knowing it before you sit across from your first client changes everything.

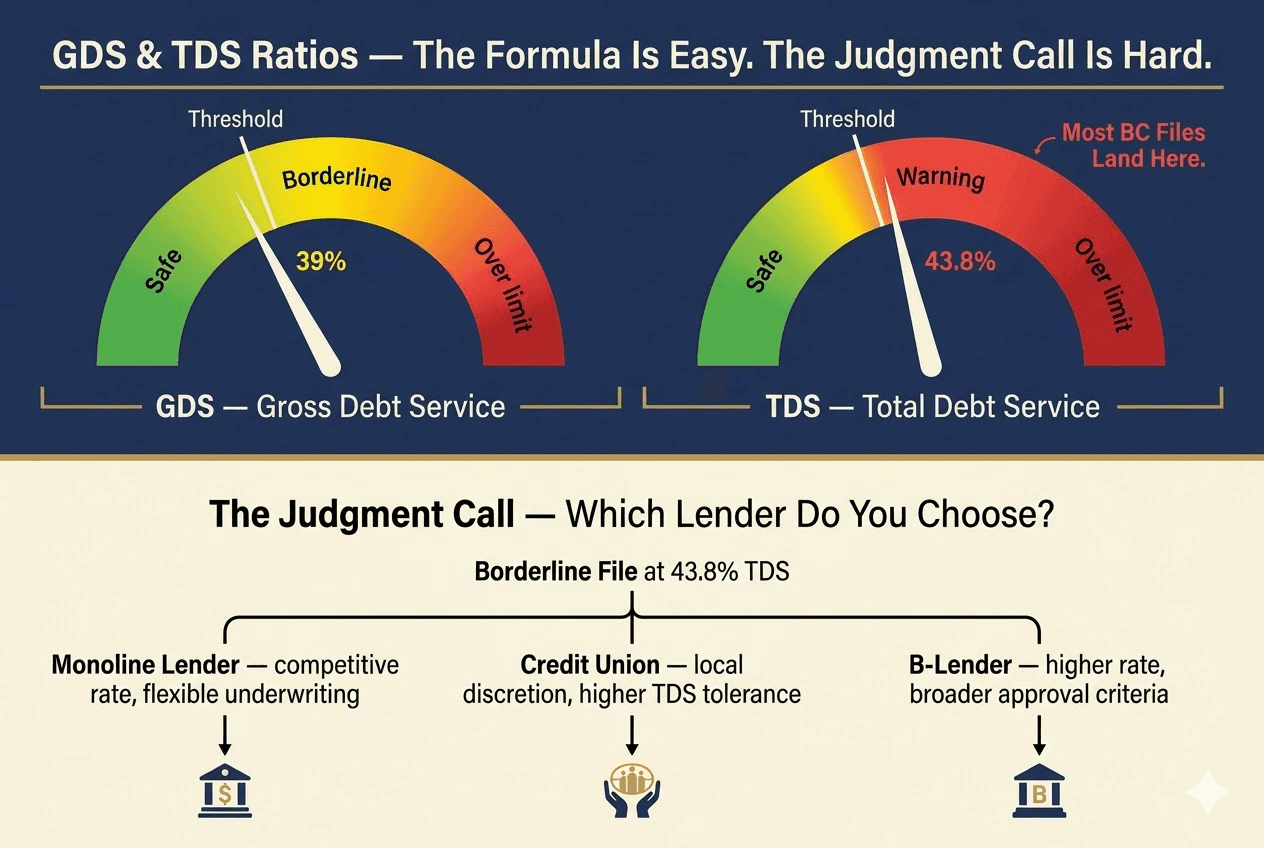

Secret 5 — GDS & TDS Ratios: The Formula Is Easy. The Judgment Call Is Hard.

The GDS and TDS formula is in the textbook. CMHC sets the standard GDS threshold at 39% and TDS at 44% for insured mortgages.

What nobody teaches is what to do when a client lands at 43.8% TDS — just under that ceiling. Do you go to a monoline lender, a credit union, or a B-lender? How do you present the file so it lands favourably?

In BC's high-price market, borderline files are not exceptions. They are the majority of deals you will actually work.

Note: The textbook teaches the formula. Real BC deals require the judgment call that comes after it.

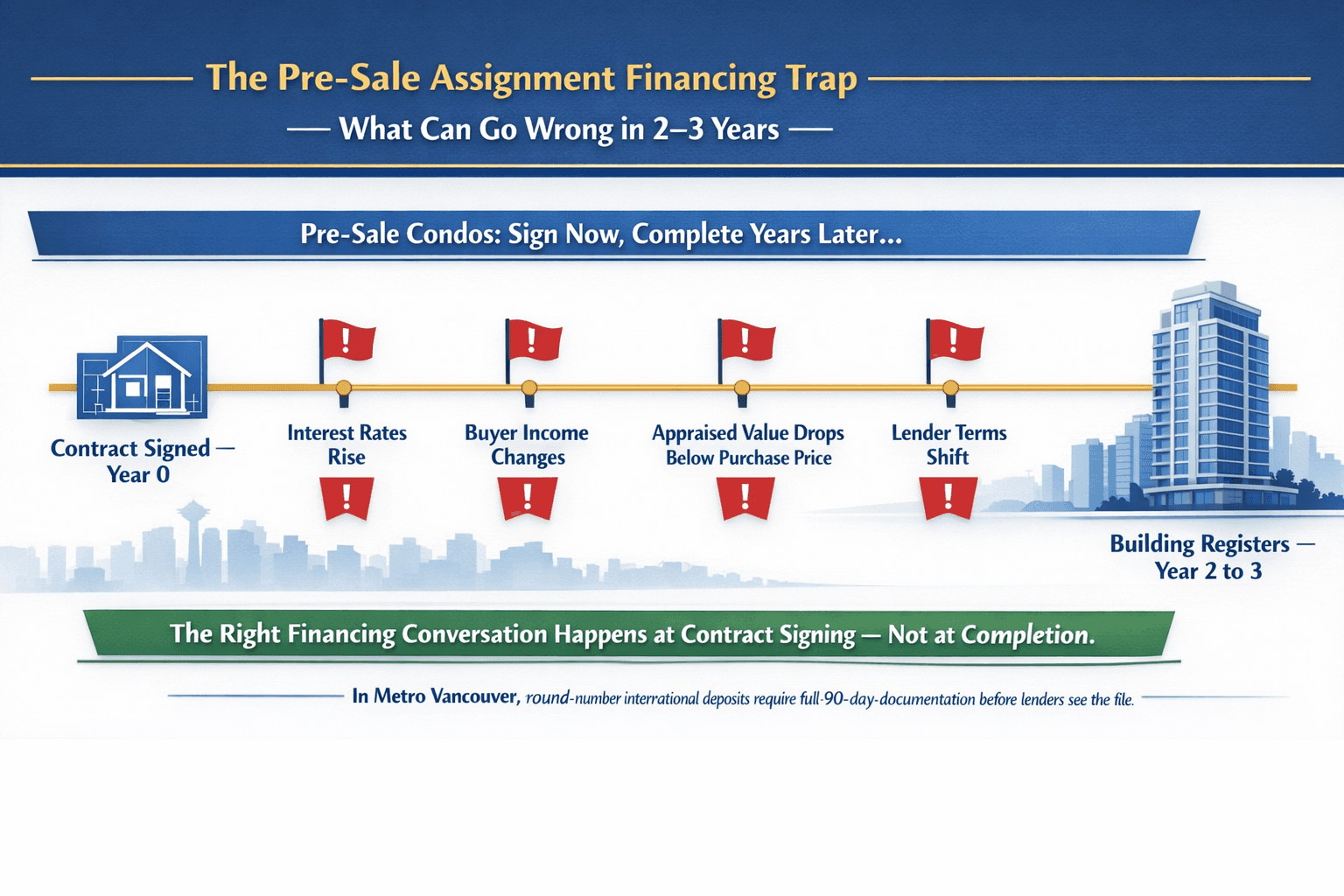

Secret 6 — The Pre-Sale Assignment Financing Trap (Vancouver's Invisible Career Risk)

Vancouver and Surrey run on pre-sale condo contracts. Buyers sign purchase agreements 2-3years before a building is completed. By the time it registers, rates may have risen, income may have changed, and the appraised value may not match the original purchase price.

Most new brokers walk into their first pre-sale deal completely unprepared because no standard curriculum addresses it. The right financing conversation needs to happen at contract signing — not at completion panic.

Note: Pre-sale assignment financing is a Vancouver and Fraser Valley market reality that is absent from any national mortgage curriculum.

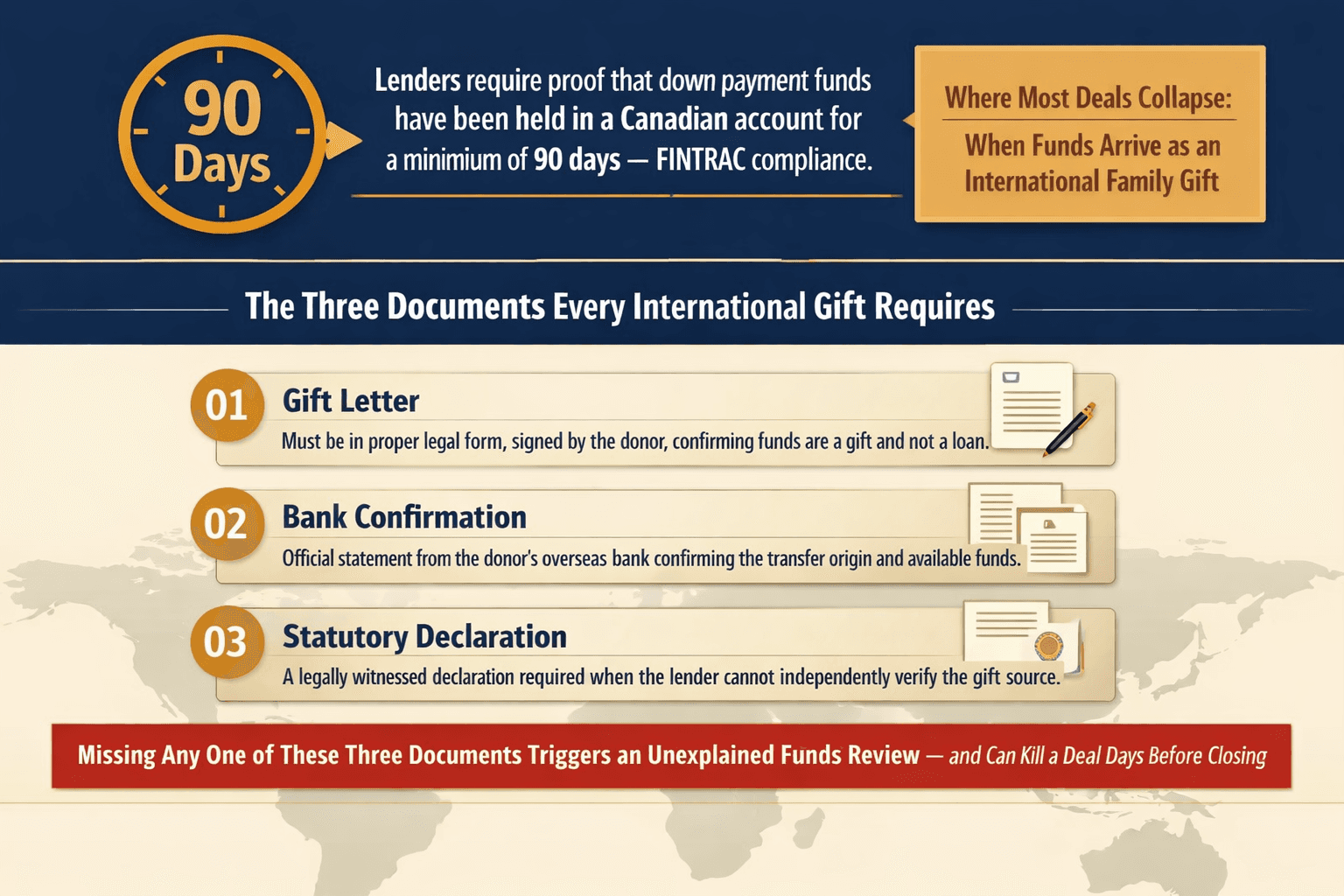

Secret 7 — The 90-Day Rule Has a Layer Nobody Explains to Newcomer Clients

Everyone knows the 90-day rule for down payments—it's a basic FINTRAC compliance requirement. The paperwork pile when funds come from overseas family, super common for Vancouver first-time buyers.

A $200,000 wire transfer from overseas requires three specific documents: a gift letter in legal form, bank confirmation from the sending party, and, in many cases, a statutory declaration. Missing any one of these triggers an unexplained funds review — and can kill a deal days before closing.

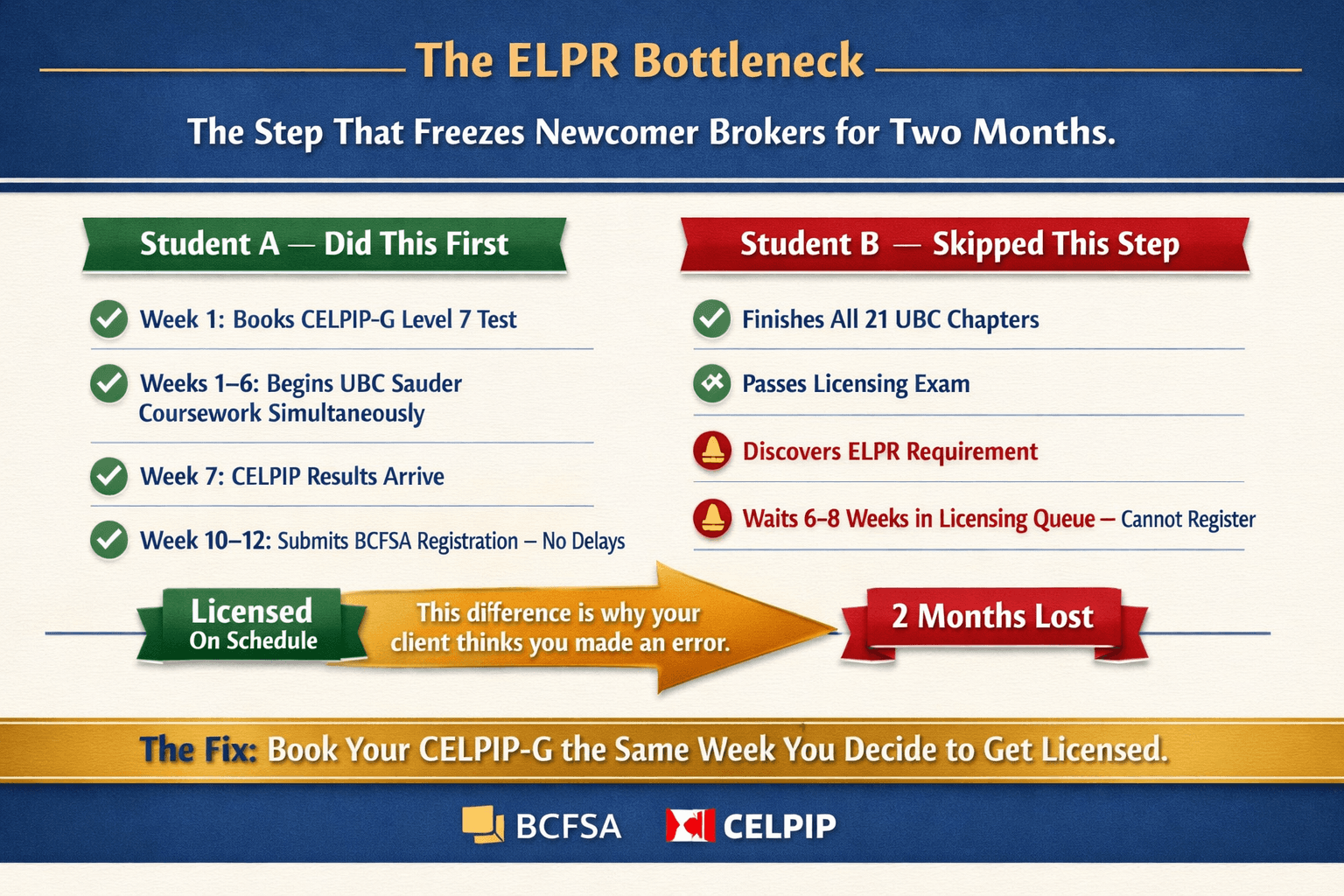

Secret 8 — The ELPR Bottleneck That Costs Newcomers Two Months of Their Career

BCFSA requires a CELPIP-G Level 7 English proficiency score before you can register as a mortgage broker in BC — if English is not your first language. Booking the test, sitting it, and receiving results takes six to eight weeks.

Students who finish all 21 UBC chapters and pass the exam without completing this first step end up frozen in a licensing queue for two months. The fix is simple: book your CELPIP-G the same week you decide to pursue licensing. Use the waiting period to begin your UBC coursework simultaneously.

Secret 9 — Semi-Annual Compounding: The Math That Embarrasses New Brokers in Front of Clients

Canadian fixed-rate mortgages compound semi-annually — not monthly like US mortgages. This means your payment calculations will never match what clients find on American mortgage calculators, and first-time buyers will sometimes challenge your numbers, convinced you made an error. You need to explain this distinction clearly, without hesitation, in plain language.

The formula is: Monthly rate = (1 + annual rate ÷ 2)^(1/6) − 1.

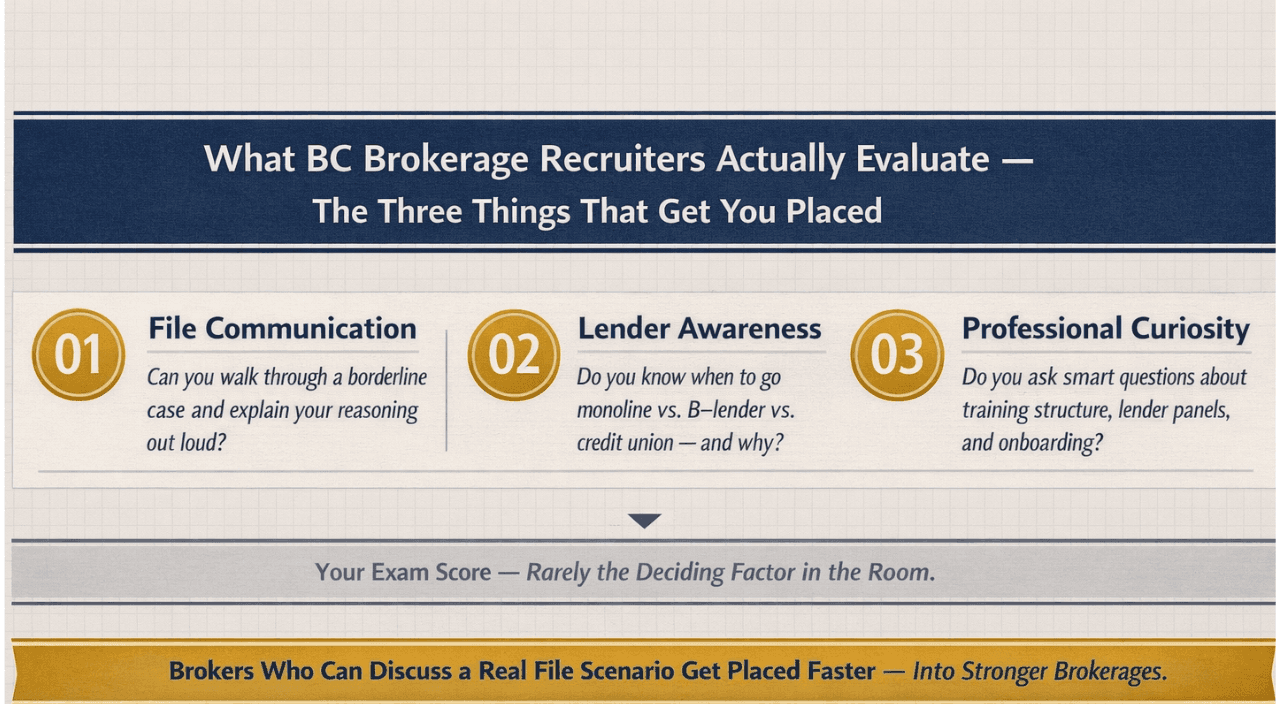

Secret 10 — What Brokerage Recruiters Actually Want (Intelligence From Our Placement Network)

BC brokerage recruiters also called Designated Individuals helps in evaluating three things fpr new applicants:

File communication (can you walk through a borderline case and explain your reasoning?)

Lender awareness (do you understand when to go monoline vs. B-lender vs. credit union?)

Professional curiosity (do you ask smart questions about training structure and lender panels?).

Your exam score is rarely the deciding factor. Brokers who can discuss a real life scenario in a recruitment conversation, not just confirm they passed a test, get placed faster and into stronger brokerages.

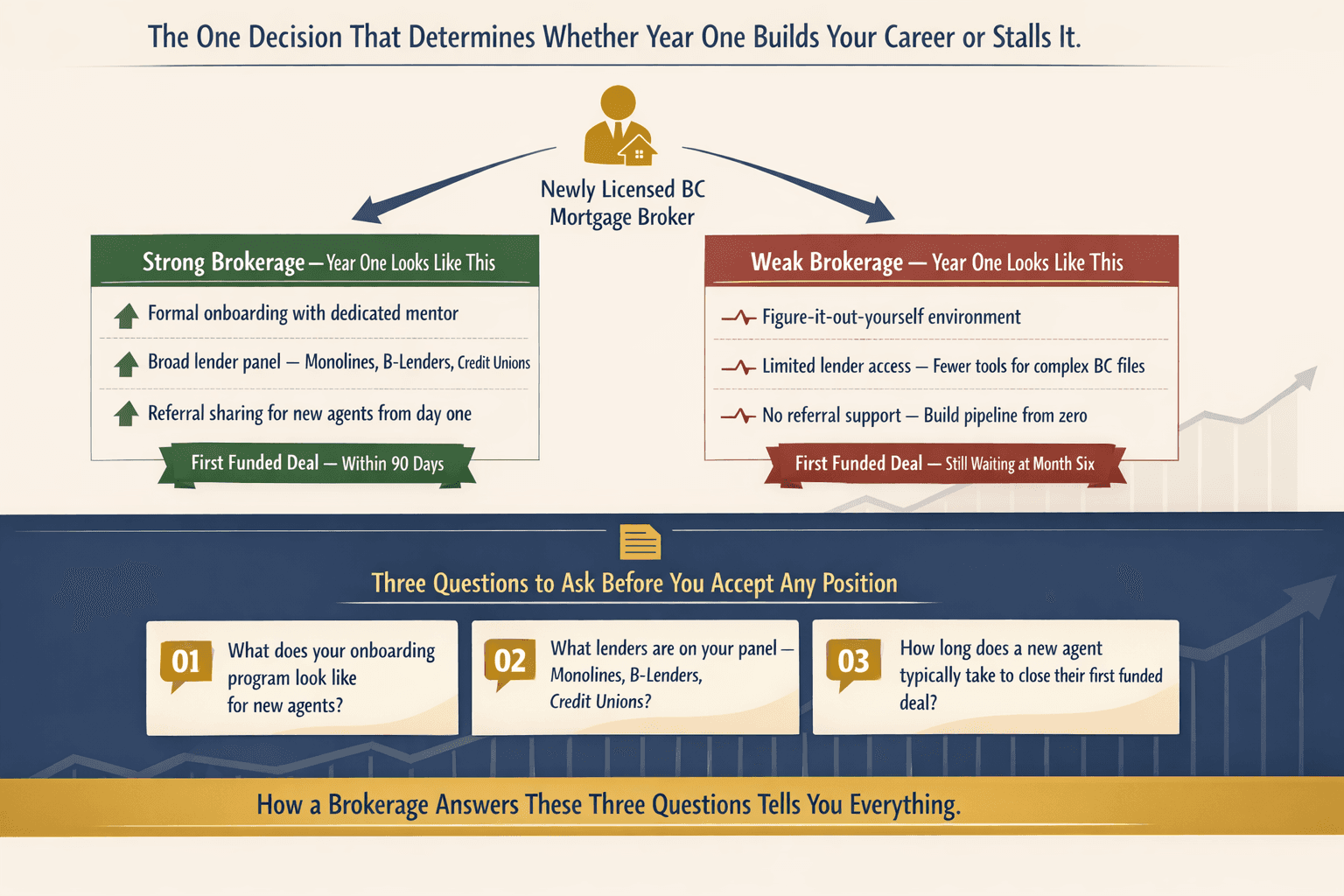

Secret 11 — The Real Reason Most New BC Brokers Struggle in Year One (And the One Decision That Prevents It)

The brokerage you join after licensing controls three things that directly determine your first-year income:

Mentorship structure (formal training vs. figure-it-out-yourself)

Lender panel access (broad lender relationships mean more tools for complex BC files)

Income timeline support (some brokerages share referrals with new agents; most don't).

Before accepting any position, ask:

What does onboarding look like?

What is your lender panel?”

How long does a new agent typically take to close their first funded deal?

How a brokerage answers those three questions tells you everything about whether year one will build your career or stall it.

Conclusion

“The textbook gets you licensed. What you just read gets you earning”.

These 11 secrets won't appear in your UBC Sauder course material. They come from 20 years of watching 10,000 BC students navigate the same path — and knowing exactly where each one stumbled.

You don't have to learn this the hard way. Start your free trial today and get the roadmap, the mentorship, and the guarantee.

FAQs

How long is the mortgage broker course in BC?

What skills do you need to be a mortgage broker?

What is changing with the Mortgage Services Act (MSA) in 2026?

In this Article

This article is Written By

Samir Nathwani

A dedicated professional committed to supporting educational progress, program development, and learner success across various career pathways.