Key Takeaways

|

BC's real estate market is booming, and mortgage brokers are earning an average of $129,346 annually.

But can you really break in? And what does it actually take?

Here's the reality: In 4–6 months and $3,500, you can get licensed by completing the UBC Sauder course, passing the BCFSA exam, and registering as a broker. The opportunity is real—but so are the challenges most people skip.

Here we have answered the questions holding you back: exact costs, realistic income timelines, exam difficulty, and 2026's regulatory changes.

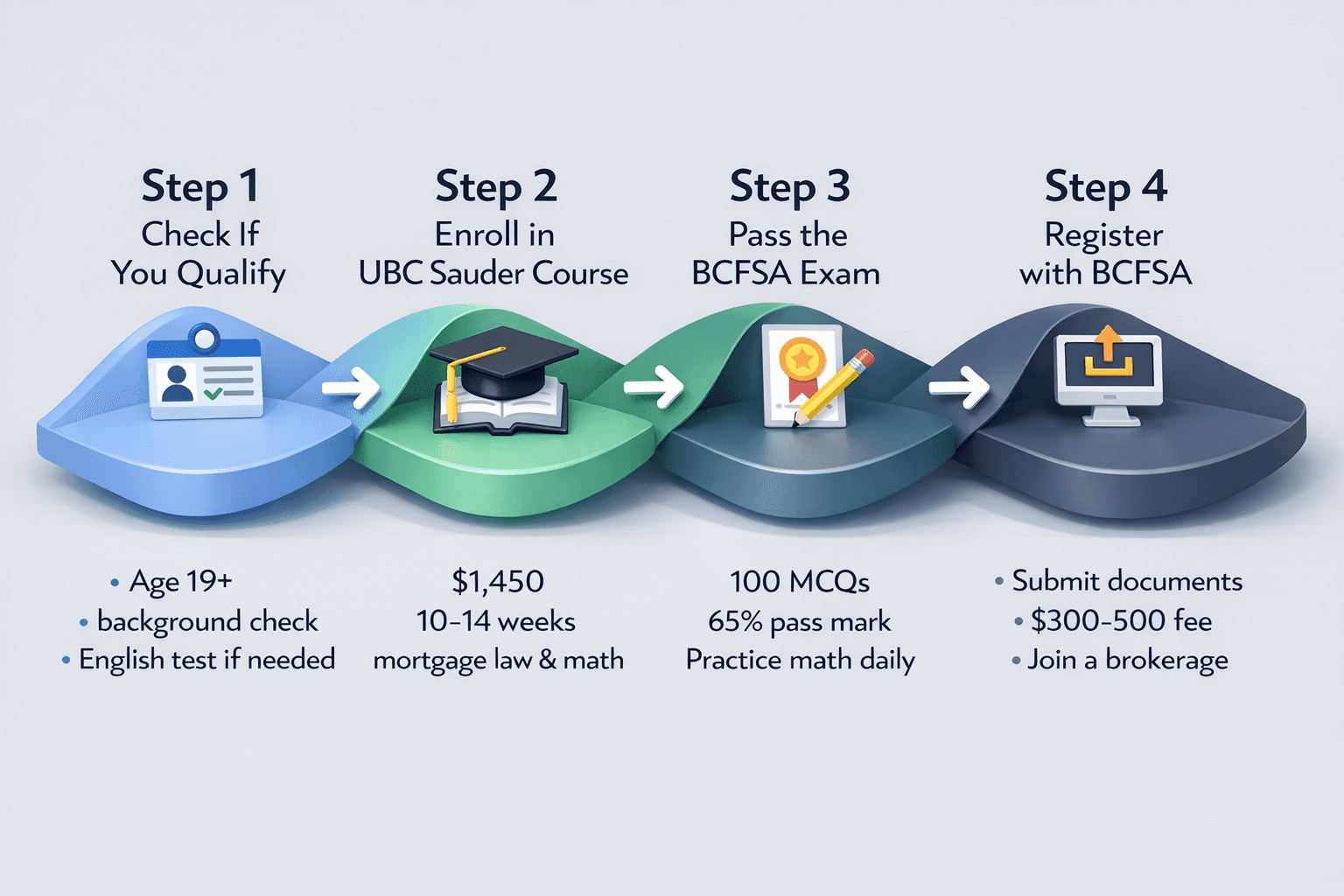

YOUR 4-STEP ROADMAP TO SUCCESS (4–6 Months)

Ready to get started? Follow this proven path to obtaining a mortgage broker license in BC.

STEP 1: CHECK IF YOU QUALIFY

Before you invest time or money, make sure you meet the basic requirements set by the BC Financial Services Authority (BCFSA):

Age & Work Status: You must be at least 19 and legally able to work in Canada.

Background Check: A certified criminal record check (within 90 days) is mandatory. Fraud, financial crimes, or serious violent offenses will disqualify you.

English Proficiency: If English isn’t your first language, you’ll need CELPIP‑General Level 7 or higher in reading, writing, listening, and speaking. Cost is about $300, with results in 2–4 weeks.

Disqualifiers: Bankruptcy within the past two years, serious convictions, or poor financial history. If you fall into these categories, real estate licensing may be a better alternative.

Action today: Order your criminal record check ($50–100). If you need CELPIP, book it immediately to avoid delays.

STEP 2: ENROLL IN UBC SAUDER COURSE

The UBC Sauder “Mortgage Brokerage in British Columbia” course is the only program approved by BCFSA.

Cost: $1,450

Duration: 10–14 weeks, self‑paced (max 2 assignments per week, 1‑year deadline)

Modules: Mortgage law, BCFSA regulations, mortgage math (GDS/TDS ratios, stress tests), lending products, underwriting, compliance, and ethics.

Key math you’ll master:

GDS (Gross Debt Service): (Mortgage + taxes + heating) ÷ Monthly income ≤ 39%

TDS (Total Debt Service): (All debt payments) ÷ Monthly income ≤ 44%

Example: A $500,000 mortgage at 5.5% over 25 years requires ~$120,000 household income to qualify.

Required tool: HP10BII+ calculator (~$50–80). You’ll use it for assignments, the exam, and daily work.

Ready to Start the Course?

Enroll in the UBC Sauder course now through Realty Course and begin your path to mortgage broker licensure. Don't delay—enroll this week to stay on the 4–6 month timeline.

Step 3: Pass the BCFSA Exam

The licensing exam is where most candidates stumble—but with the right prep, you’ll pass.

Format: 100 multiple‑choice questions, 3 hours, 65% pass mark.

Cost: $200 per attempt.

Why Candidates Fail

Skipping mortgage math practice — even though math is roughly 20% of the exam, it requires consistent daily drilling to execute accurately under time pressure.

Memorising terminology instead of understanding concepts..

Avoiding mock exams until it is too late to identify weak areas.

Maximize your exam pass rate: Get exam prep materials and practice tests at Realty Course's Mortgage Broker Program. Mock exams and detailed answer explanations will help you identify weak areas before test day. |

STEP 4: REGISTER WITH BCFSA

Once you pass the exam, you must register with BCFSA before you can legally work as a sub-mortgage broker in BC.

Process: Log into the BCFSA IRIS portal and upload your exam certificate, background check, valid ID, and CELPIP results (if applicable). Payment is made directly through the portal using Visa or Mastercard (credit or debit).

Your personal registration fee: As a sub-mortgage broker, you are responsible for paying your own registration fee directly to BCFSA — this is not covered by your sponsoring brokerage.

Brokerage Licensing Fees (Paid by the Brokerage, Not You)

Registrant Type | Current Fee (Mortgage Brokers Act) | New Fee from Oct 13, 2026 (Mortgage Services Act) |

Sub-Mortgage Broker (you) | $1,500 | $2,100 |

Mortgage Broker / Brokerage | $1,900 | $3,100 |

Branch Office | $200 | $3,100 |

Note on 2026 Regulatory Changes: The new Mortgage Services Act (MSA) replaces the current Mortgage Brokers Act (MBA) on October 13, 2026. BCFSA is leading the transition, and new licensing education programs will launch in mid-2026. If you complete the current MBA program before summer 2027, you'll also need short transition training. Starting after October 2026, only the new MSA program will apply. |

STARTING YOUR CAREER AT A BROKERAGE

With your licence in hand, the next phase is finding a brokerage to sponsor and support you. You cannot operate independently as a submortgage broker — joining a licensed brokerage is a legal requirement, and the right choice here will significantly impact your first-year income and career trajectory.

Choosing the Right Brokerage

Interview multiple brokerages before committing. Here is what to evaluate:

Commission split: Aim for 60% or higher to start. A 60/40 or 70/30 split (you keep 60–70%) is standard and fair.

Desk fee: Expect $500–$1,500 per month. Anything above $1,500 per month with no mentorship support is a red flag.

Mentorship: Critical in your first 90 days. Confirm there is a dedicated mentor assigned to new brokers.

Lender relationships: 15+ active lender relationships are the industry standard. Fewer limits the products you can offer clients.

Training support: Look for structured onboarding, help with lender portal access, and ongoing education.

Red Flags to Avoid

Commission split below 50%

High desk fees with no mentorship or training support

Fewer than 10 lender relationships

No formal onboarding program for new brokers

What to Expect in Your First 90 Days

The first three months are about building foundations, not cashing large cheques. Here is a realistic picture:

Days 1–30 | Days 31–60 | Days 61–90 |

Learn lender portals (5–15 systems) | First deal may close — real commission! | Build referral relationships |

Zero income — you are training | Earn $2,500–$6,000 gross | 2–4 deals in pipeline |

Get assigned a mentor | Manage appraisals, conditions, closing | Identify your specialty niche |

Attend lender meetings | Learn how clients actually behave | Double down on top referral sources |

Income expectation: After 90 days, most brokers have earned $5,000–$20,000 gross ($3,000–$12,000 net). This is not yet enough to live on comfortably — treat this period as investment in your pipeline, not your payday.

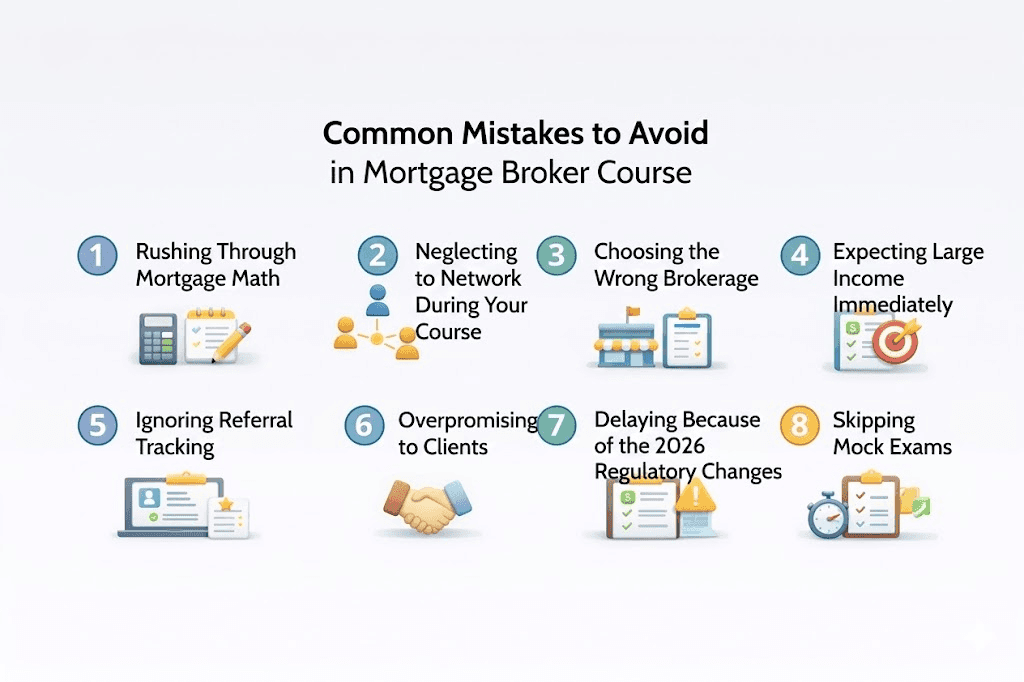

Practical Tips for Mortgage Broker Success

1. Rushing Through Mortgage Math

Math makes up roughly 20% of the BCFSA exam but requires consistent practice to execute quickly and accurately under timed conditions. Do not underestimate it.

Fix: Dedicate focused daily practice sessions with your HP10BII+ throughout weeks 3–8 of exam prep.

2. Neglecting to Network During Your Course

Referrals drive approximately 80% of mortgage business in BC. Most new brokers graduate with zero leads because they waited too long to start building relationships.

Fix: Start networking from week 8 of your course onward. Connect with real estate agents, attend lender events, and join local professional groups. Track every contact from day one.

3. Choosing the Wrong Brokerage

A brokerage with poor commission splits, limited lenders, or no mentorship can stall your career significantly in the critical first year.

Fix: Research thoroughly. Interview at least three brokerages before deciding. Prioritise mentorship, fair splits, and lender breadth over proximity or brand name.

4. Expecting Large Income Immediately

Year 1 gross earnings typically range from $50,000–$80,000, not $100,000+. The first 90 days usually mean $0 while you are training.

Fix: Plan your finances before you start. Maintain a personal financial buffer of at least 3–4 months of living expenses. Treat Year 1 as pipeline-building, not payday.

5. Ignoring Referral Tracking

Without a system, you waste time on low-quality leads and lose visibility into what is actually driving your business.

Fix: Use a simple CRM or even a spreadsheet from day one. Log every referral, note the quality and source, and double down on your highest-performing referrers.

6. Overpromising to Clients

Guaranteeing approval rates or rates you cannot deliver destroys trust and creates compliance risk.

Fix: Be transparent about options, timelines, and scenarios. Honesty builds the repeat and referral business that drives long-term income growth.

7. Delaying Because of the 2026 Regulatory Changes

The Mortgage Services Act (MSA) replaces the MBA on October 13, 2026. Starting after the transition could mean extra training requirements and delays.

Fix: Enrol in the UBC course now and monitor BCFSA communications regularly for updates on the transition process.

8. Skipping Mock Exams

Last-minute cramming without full practice exams is one of the most reliable ways to fail.

Fix: Complete at least three full practice exams before your test date. Book your exam immediately after finishing your course assignments to maintain momentum.

Conclusion

Mortgage brokering in BC is a clear path: qualify, complete the UBC course, pass the exam, and join a brokerage. Costs are about $2,500, timeline 4–6 months. Expect $0 income in month one, $5k–$20k gross by 90 days, and an average base salary of $88,913 in Year 1. The real challenge is networking, referral tracking, and financial discipline. With focus and ethics, income accelerates in Years 2–3. Begin today to avoid delays from the upcoming 2026 regulatory changes.

FAQs

How much will I earn first month?

Can I do this part-time?

What if I fail the exam?

Mortgage broker or real estate agent?

Do I need experience?

In this Article

This article is Written By

Samir Nathwani

A dedicated professional committed to supporting educational progress, program development, and learner success across various career pathways.